I've become numb a long time ago ... but seeing these programs and "solutions" one after the other is simply.... I don't have words. Just enjoy - last week we mentioned how some states had created a work around to use the tax REBATE (i.e. AFTER you buy the home you get the handout) as a substitute for a down payment and closing costs [May 8: Minyanville - Subprime Lending is Back with a Vengeance]

In an effort to boost home buying -- even for marginally qualified borrowers -- a number of states are finding creative ways to advance the tax credit to buyers on the day they get their new keys, rather than having to wait for next year's refund check. This allows buyers to pay for things like closing costs, mortgage points - or even the down payment.

Well folks - it did not take long... the early results of letting people who cannot even find enough money to put 3.5% down into the housing market must of been spectacular. Because in just the blink of an eye this "adjustment" to what Congress originally approved, has now become the federal standard.

(May 12, 2009) Shaun Donovan, secretary of the U.S. Department of Housing and Urban Development, said that the Federal Housing Administration is going to permit its lenders to allow homeowners to use the $8,000 tax credit as a downpayment.

Secretary Donovan said that important changes, which the National Association of Realtors(R) has been calling for, will help consumers purchase a home. "We all want to enable FHA consumers to access the home buyer tax credit funds when they close on their home loans so that the cash can be used as a downpayment," Donovan said.

According to Donovan, the FHA's approved lenders will be permitted to "monetize" the tax credit through short-term bridge loans. This will allow eligible home buyers to access the funds immediately at the closing table.

This is the same FHA we posted last week would cause the next housing bust [May 6: WSJ - FHA Loans, the Next Housing Bust]

Last year banks issued $180 billion of new mortgages insured by the FHA, which means they carry a 100% taxpayer guarantee. Many of these have the same characteristics as subprime loans: low downpayment requirements, high-risk borrowers, and in many cases shady mortgage originators. FHA now insures nearly one of every three new mortgages, up from 2% in 2006.

... taxpayer losses are mounting on its $562 billion portfolio. According to Mortgage Bankers Association data, more than one in eight FHA loans is now delinquent -- nearly triple the rate on conventional, nonsubprime loan portfolios. Another 7.5% of recent FHA loans are in "serious delinquency," which means at least three months overdue.

Because FHA also allows borrowers to finance closing costs and other fees as part of the mortgage, the purchaser's equity can be very close to zero.

So let's wrap this up and put a bow on it. Effectively the US government is going to allow people with "3.5% down" (now covered by the tax payers gift of $8000) to enter into agreements of sub 5% mortgage rates, to FICO scores as low as 620. As long as its your first home. Closing costs? Remembers the FHA allows people to finance that... you don't need to have it on you.

To put that in perspective this means, based on the median home price in America - about 70% of homes are now available to home buyers for less upfront than a rental. In a rental you at least need to save enough to put down a security deposit. Under this innovative program (that was not the original intent of the legislation) $8000 can finance 3.5% down on up to a $228,000 home.

Anyone who can make the monthly payments from there now is welcome to join the home ownership class. Or if you really don't care about your 620, 630 FICO score you can basically get into one of these homes, not make a single payment and live rent free from 12-18 months before they get around to foreclosing on you (which many banks are dragging their feet on).

And if the home value goes down even 1% and you find yourself immediately underwater? You walk away and send the keys to the US taxpayer - we're going to pay for it on the back end as well as the front end.

This is what was done in the auto industry - it's called pulling forward demand with greater and greater incentives (0% interest rates for multiple years, $4K, $5K, $6K rebates). Now we pulled almost all natural demand for home buyers that should of been arriving in 2008-2009 into 2006-2007. So you have to create an even stronger drug when you can rustle up enough home buyers. And here we are.... and when home data "drops at a slower rate than the previous period" we can rally on "2nd derivative improvement"... failing to mention whom is bearing the costs for that improvement.

Am I surprised? No. It's all Groundhog Day at this point - each program begins to sound like the other. Common theme is taxpayer handouts and taxpayers bearing risk - Kick the Can policies. In my predictions piece for 2009 I wrote things would get so desperate... err, correction - I wrote green shoots would be so plentiful that:

But larger than that - my prediction is Fannie/Freddie and then above and beyond that, for people who do not have 20% down and won't pay for insurance, the FHA - will wage a war against current mortgages. We'll see interest rate buydowns, we'll see principal reductions, we'll see anything and everything that basically gives a big (bleep) you to people who have been honoring the system. In return we will tell those people, well if your neighbor's house goes into foreclosure we will all suffer, so it's a necessary evil.

By the back half of 2009, refinancing will reach levels (and above) seen in the bubble years of 2005-2006. Obama & Co will also come up with myriad plans for buyers to suck up excess inventory - the government will be our partner. Nothing should surprise you - this will be an all out assault - we are already seeing the first inane ideas such as no appraisal refinances. The "private" mortgage industry will be almost completely crowded out as no one can compete with what the government will offer.

Source

May 24, 2009

Finding the 'Perfect Time' to Buy a Home

In the kitchen, it's common wisdom that you don't try to catch a falling knife. But in real estate markets that have recently seen double-digit declines, many buyers are anxious to catch the equivalent of a falling house.

|

AP |

They're betting they can buy property at or near its cyclical bottom by scoping out distressed but fundamentally desirable neighborhoods, floating lowball offers and focusing on bank-owned homes.

It's easy to understand why, given the property values in some of the nation's hardest-hit real estate markets. Home prices in the five worst-performing major metropolitan areas -- Las Vegas, Miami, Phoenix, San Francisco and San Diego -- are down more than 40 percent from their peaks, according to the S&P/Case-Shiller Home Prices Indices. With interest rates for government-backed mortgages at record lows, monthly payments for owner-occupants are at their most affordable levels in years.

Nonetheless, economists and veteran real estate investors say market timing is a risky proposition.

"The odds of you timing the bottom perfectly are pretty low," says Rick Sharga, vice president of marketing at RealtyTrac, a foreclosure data provider. "If you're that good, you should be playing the stock market every day."

Although the current buyer's market may look attractive, rising unemployment rates and persistently high foreclosure rates add pressure on the battered housing sector. Housing Predictor, a forecasting Web site, predicts that 25 housing markets, from Las Vegas to Seattle, will see declines between 14 percent and 27 percent this year.

Sharga sees little reason for prospective owner-occupants in most markets to back away from buying an affordable property. Prices could drop further, he says, but the worst has probably passed. Additionally, historically low mortgage rates and tax incentives for new buyers probably won't last much longer.

Still, real estate is the ultimate local commodity, and some markets will be closer to bottom than others, so prospective buyers looking to protect themselves against further price declines need to consider local economic conditions. Before finalizing a purchase, real estate experts advise that price-sensitive buyers check these five critical factors.

| Mortgages |

|

| ||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||

|

Look for positive indicators: Rising prices are the most obvious indicator of a market recovery, but they’re also evidence that the cycle has already passed its low point. In still-declining markets, however, you can still find other positive indicators. David Kendall, a Realtor in Oakland, Calif., says he's encouraged to see a rise in sales volumes in some hard-hit ZIP codes, indicating that buyers are comfortable with current prices. Other potential turnaround signs include a drop in the number of days that homes sit on the market and an uptick in competitive bidding for compellingly priced properties.

Be aware of "shadow inventory": Banks often don't want to put their entire real estate inventory on the market at once. Doing so can depress prices, particularly in neighborhoods that have not yet seen a high number of foreclosure sales. Because of several factors -- including the recently expired moratorium on home repossessions and anticipation around new federal mortgage assistance programs -- banks have been allowing such "shadow inventory" to build up, says Chris Matty, marketing director at ForeclosurePoint, which publishes foreclosure data. "There's a huge pool of inventory and distressed homes that have not made it to the market yet," he says. "But eventually that has to come."

May 23, 2009

FHA Decision Could Benefit Home Buyers, Builders

The U.S. government gave ailing home builders a ray of hope, although it also raised concerns lending mistakes that fueled the housing boom - and bust - could be repeated.

The Department of Housing and Urban Development's Federal Housing Administration is paving the way for first-time buyers to tap a federal tax credit of up to $8,000 for a downpayment. The announcement, made Tuesday before several thousand real-estate agents attending the National Association of Realtors' Real Estate Summit, could prove a game changer for the sluggish housing ... continue reading

The Department of Housing and Urban Development's Federal Housing Administration is paving the way for first-time buyers to tap a federal tax credit of up to $8,000 for a downpayment. The announcement, made Tuesday before several thousand real-estate agents attending the National Association of Realtors' Real Estate Summit, could prove a game changer for the sluggish housing ... continue reading

May 22, 2009

Is buying a home with a friend a good idea?

What do you do if you want to buy a house but can't afford it? Ever thought about buying a home with a friend?

More and more, friends are teaming up to do just that. Time Magazine recently dubbed the term 'Co-Ho,' for communal homeowners.

While it can save you money and help build equity, there are some pitfalls. But a couple of friends who partnered up to purchase a home together say if you do it right, it can work.

Good friends Jaime Arb-Haessig and Sarah Marzolf share a duplex in northeast Portland and by 'sharing,' we mean the loan, the taxes, the maintenance and the utility bills. Both are in their early 30s and figured they would pool their money to give them greater buying power.

"I work at a non-profit, so I would not be able to afford to buy a house by myself," said Marzolf.

"When I was looking to buy a home, I realized I couldn't buy into a neighborhood I wanted to live in," said Arb-Haessig.

But owning a home together meant having their finances and assets tied together and the bank doesn't care who is late with the check. If one person defaults on the loan, both their credit ratings could take a hit. The thought of that didn't sit well with their families at first.

"Hell no was my parents' reaction," said Marzolf. "They're like 'that's not a good idea, you don't know what's going to happen.' "

But the contract was very specific and included everything from how long they plan to keep the property, how it will be sold, how to handle repairs, what happens if one moves out, what happens when one of them dies and even naming a third-party mediator in case something turns ugly.

The two don't anticipate anything going wrong and said their living arrangement has actually helped their friendship.

"We've stayed closer than we would have otherwise," said Arb-Haessig. "And we're more up on what's going on in each other's lives."

They also have other contingencies in place. They opened a joint rainy day account for emergency repairs or if someone is a little late on a payment one month. Arb-Haessig also recommends consulting a real estate attorney.

Source

May 21, 2009

Not-So-Tricky Split: The Home Buyer Tax Credit

The new-and-improved version of the First-Time Homebuyer Credit offers rookie home buyers (or those who simply haven't owned a home in the past three years) a chance to get a federal income tax credit of up to $8,000. Thanks to this year’s Stimulus Act, you don't have to repay the credit like you did with last year’s version.

Even better, the IRS says unmarried individuals can team up on a home purchase and then share the credit. If you're thinking of going this route, here's what you need to know to get the best tax-saving results:

How Much You'll Get

The updated First-Time Homebuyer Credit can be applied to purchases of homes that occur between Jan. 1, 2009, and Nov. 30, 2009. The maximum credit equals the lesser of 10% of the purchase price of a principal residence or $8,000. Or, in the case of married individuals who file separately, $4,000. (These amounts are up from the $7,500 and $3,750 limits for purchases that occurred between April 9 and Dec. 31 of last year.)

There are some catches, however. The credit is phased out (reduced or completely eliminated) if your modified adjusted gross income (MAGI) is too high. (For this purpose, MAGI means the adjusted gross income figure reported on the last line on page 1 of your Form 1040 increased by certain income from outside the U.S. that is exempt from taxation.)

For married joint filers, the credit is phased out when the MAGI is between $150,000 and $170,000. For unmarried individuals and married individuals who file separately, the credit is phased out between MAGI of $75,000 and $95,000.

You can use the credit to offset your entire federal income tax bill, including any alternative minimum tax (AMT). Since the credit is refundable, you can collect any amount left over after your tax bill has been reduced to zero in cold, hard cash.

Eligibility

The credit is only available to buyers who have not owned a principal residence in the U.S. during the three-year period that ends on the purchase date for the home. That home must serve as the new principal residence.

If you’re married, both you and your spouse must pass the three-year test (whether or not you file jointly). If you’re unmarried, and you team up with another person to buy a home that serves as the new principal residence for you both and you both pass the three-year test, then you can share the credit. If only one of you passes the three-year test, only that person can claim the credit.

Unmarried Buyers Can Share the Credit

Say two (or more) unmarried individuals buy a home together that serves as their new principal residence. Assuming each person passes the three-year test and they jointly own the property as tenants in common or as joint tenants, they can pretty much share the credit any way they choose, according to IRS Notice 2009-12. However, the total credit is still limited to the lesser of 10% of the purchase price or $8,000. And the credit allocated to each person is still subject to the phase-out rule, based on MAGI. Although the IRS doesn’t actually say so, it appears you can’t claim a credit that exceeds your share of the purchase price (including your share of any mortgage debt). Here’s an example to illustrate the possibilities.

Example: Say you and your significant other jointly buy a home for $150,000 in June of this year and you both pass the three-year test. You pay 60% of the cost, and your partner pays 40%. The available credit for this purchase is $8,000 (lesser of 10% of the purchase price or the $8,000 credit ceiling). You and the other person could agree to share the credit 60/40 to reflect your shares of the purchase price. But if the other person's MAGI is too high to claim the credit and yours is not, then it makes good tax-saving sense to have the entire $8,000 allocated to you. On the flip side, if your MAGI is too high, the entire $8,000 could be allocated to the other person. Or you could split the credit 50/50, or 75/25, or 25/75, or whatever allocation suits the two of you best. Anything you decide is OK with IRS.

Word of Caution: Credit Must Be Repaid in Some Circumstances

Under last year’s version of the First-Time Home Buyer Credit, those who bought homes between April 9, 2008, and Dec. 31, 2008, were generally required to repay the credit over 15 years. The Stimulus Act eliminated the repayment rule -- in most cases. However, the repayment rule can still hit you if you sell the home you buy in 2009 within three years of the purchase date or stop using the home as your principal residence during that time. If either of those events occurs, you generally must repay your entire credit when you file your Form 1040 for the year during which the triggering event occurs (no 15-year repayment deal for you

Source

Even better, the IRS says unmarried individuals can team up on a home purchase and then share the credit. If you're thinking of going this route, here's what you need to know to get the best tax-saving results:

How Much You'll Get

The updated First-Time Homebuyer Credit can be applied to purchases of homes that occur between Jan. 1, 2009, and Nov. 30, 2009. The maximum credit equals the lesser of 10% of the purchase price of a principal residence or $8,000. Or, in the case of married individuals who file separately, $4,000. (These amounts are up from the $7,500 and $3,750 limits for purchases that occurred between April 9 and Dec. 31 of last year.)

There are some catches, however. The credit is phased out (reduced or completely eliminated) if your modified adjusted gross income (MAGI) is too high. (For this purpose, MAGI means the adjusted gross income figure reported on the last line on page 1 of your Form 1040 increased by certain income from outside the U.S. that is exempt from taxation.)

For married joint filers, the credit is phased out when the MAGI is between $150,000 and $170,000. For unmarried individuals and married individuals who file separately, the credit is phased out between MAGI of $75,000 and $95,000.

You can use the credit to offset your entire federal income tax bill, including any alternative minimum tax (AMT). Since the credit is refundable, you can collect any amount left over after your tax bill has been reduced to zero in cold, hard cash.

Eligibility

The credit is only available to buyers who have not owned a principal residence in the U.S. during the three-year period that ends on the purchase date for the home. That home must serve as the new principal residence.

If you’re married, both you and your spouse must pass the three-year test (whether or not you file jointly). If you’re unmarried, and you team up with another person to buy a home that serves as the new principal residence for you both and you both pass the three-year test, then you can share the credit. If only one of you passes the three-year test, only that person can claim the credit.

Unmarried Buyers Can Share the Credit

Say two (or more) unmarried individuals buy a home together that serves as their new principal residence. Assuming each person passes the three-year test and they jointly own the property as tenants in common or as joint tenants, they can pretty much share the credit any way they choose, according to IRS Notice 2009-12. However, the total credit is still limited to the lesser of 10% of the purchase price or $8,000. And the credit allocated to each person is still subject to the phase-out rule, based on MAGI. Although the IRS doesn’t actually say so, it appears you can’t claim a credit that exceeds your share of the purchase price (including your share of any mortgage debt). Here’s an example to illustrate the possibilities.

Example: Say you and your significant other jointly buy a home for $150,000 in June of this year and you both pass the three-year test. You pay 60% of the cost, and your partner pays 40%. The available credit for this purchase is $8,000 (lesser of 10% of the purchase price or the $8,000 credit ceiling). You and the other person could agree to share the credit 60/40 to reflect your shares of the purchase price. But if the other person's MAGI is too high to claim the credit and yours is not, then it makes good tax-saving sense to have the entire $8,000 allocated to you. On the flip side, if your MAGI is too high, the entire $8,000 could be allocated to the other person. Or you could split the credit 50/50, or 75/25, or 25/75, or whatever allocation suits the two of you best. Anything you decide is OK with IRS.

Word of Caution: Credit Must Be Repaid in Some Circumstances

Under last year’s version of the First-Time Home Buyer Credit, those who bought homes between April 9, 2008, and Dec. 31, 2008, were generally required to repay the credit over 15 years. The Stimulus Act eliminated the repayment rule -- in most cases. However, the repayment rule can still hit you if you sell the home you buy in 2009 within three years of the purchase date or stop using the home as your principal residence during that time. If either of those events occurs, you generally must repay your entire credit when you file your Form 1040 for the year during which the triggering event occurs (no 15-year repayment deal for you

Source

May 11, 2009

ARMed and underwater Refinancing is still possible under president's program

Question: I have a problem. Like most people out there, my mortgage is underwater. However, I have a double negative in that I bought my home in late June 2005 with an adjustable-rate mortgage with the idea of refinancing after three years.

Now, the economy has taken a plunge, along with the value of my home, which I purchased for $129,000 and is now worth $110,00-$115,000. My lender will allow borrowers such as me to refi only twice. I have gone that route once before, and I'm afraid to go there again because if I refi too early, I won't be able to do it again. My payments are $1,186 a month on a 8.625% interest rate and that hurts!

I live in a low-income area. I have spoken to another bank, which tells me my wife and I are qualified for an FHA loan. Both of us have good jobs and make enough money to cover the mortgage. But we feel its time to switch to a fixed-rate loan. So far, no lender has been able to help us.

Answer: You seem to be an excellent candidate for President Obama's Making Home Affordable program. But before you go there, I'd say that if your current lender is willing to refinance you out of an ARM into a fixed-rate mortgage, go for it. I doubt rates are going to fall much more than they already have, so I wouldn't be afraid to pull the trigger a second time because it's "too early."

A Santa Barbara wildfire forces thousands to evacuate their homes and California Gov. Arnold Schwarzenegger declares a state of emergency. Video courtesy of Fox News.

There is nothing wrong with grabbing a rate in the 5% range right now, especially if it gives you payments you can afford. My gosh, that's better than a 3.5 point difference. So in your case, the second time could be a charm.

If you are not successful, check out www.makinghomeaffordable.gov, which outlines the administration's plan to help stabilize the housing market by reducing the mortgage payments of up to 9 million eligible homeowners.

The refinance portion of the effort gives up to 5 million owners with loans owned or guaranteed by either Fannie Mae or Freddie Mac an opportunity to trade in their loans for ones that are easier on their pocketbooks. And the loan modification part commits $75 billion to keep as many as 4 million other families in their homes by preventing avoidable foreclosure.

The Web site has detailed information about these programs along with self-assessment tools and calculators to empower borrowers with the resources they need to determine whether they might be eligible for a modification or a refinance under the program. Check out the Making Home Affordable site.

Borrowers also can use the site to connect to free counseling resources to answer any questions they may have about their own personal situations. You'll also find a checklist of key documents and materials to have ready when making that important call to your lender as well as FAQs from borrowers in similar circumstances.

Q: I enjoyed your article on tax credits for energy efficient home improvements. The question I have is, do the credits phase out at higher income levels like so many of the recent tax rebates and credits (typically over $75,000).

A: Good news. There are no income limitations on the energy credits. So feel free to spend away.

Q: Great article on reverse mortgage for seniors who want to scale down the housing ladder. What happens to the lower property tax basis on the first house, the one in California? Who pays the property tax bill, and could they have used the lower or carryover basis of the old property tax basis since they over 55? See previous Realty Q&A.

A: I'm an East Coast guy who doesn't know all that much about the Left Coast. So I turned your question over to Robert D. Yeary, CEO of Reverse Mortgage Solutions. The Spring, Tex., firm has developed a specialized, state of the art system to service reverse mortgages in all jurisdictions. Here's his response:

"In California, you can transfer your old tax base to a new house, provided the county in which you purchase your new home allows that transfer. Not all counties do that. But even in jurisdictions that do allow a transfer, if you pay more for the new house, you can only transfer the tax base if the purchase price is no greater than 105% of the amount for which you sold your previous residence. If you wait a full year after the sale of your home, you can transfer 110% of the selling price."

If the new house is considerably less expensive that the home you sold, Yeary suggests considering what the property tax would be without transferring the lower basis to the new place.

"Surprisingly," he says, "in California, real estate taxes are fairly low thanks to Proposition 13. Taxes are set at the time you purchase the home and can go up only so much every year. There are plenty of houses worth $500,000 or more in California with low tax bases because they were purchased years ago for $35,000."

Yeary also notes that the Golden State offers several tax relief program for low and moderate-income seniors.

Source

Now, the economy has taken a plunge, along with the value of my home, which I purchased for $129,000 and is now worth $110,00-$115,000. My lender will allow borrowers such as me to refi only twice. I have gone that route once before, and I'm afraid to go there again because if I refi too early, I won't be able to do it again. My payments are $1,186 a month on a 8.625% interest rate and that hurts!

I live in a low-income area. I have spoken to another bank, which tells me my wife and I are qualified for an FHA loan. Both of us have good jobs and make enough money to cover the mortgage. But we feel its time to switch to a fixed-rate loan. So far, no lender has been able to help us.

Answer: You seem to be an excellent candidate for President Obama's Making Home Affordable program. But before you go there, I'd say that if your current lender is willing to refinance you out of an ARM into a fixed-rate mortgage, go for it. I doubt rates are going to fall much more than they already have, so I wouldn't be afraid to pull the trigger a second time because it's "too early."

A Santa Barbara wildfire forces thousands to evacuate their homes and California Gov. Arnold Schwarzenegger declares a state of emergency. Video courtesy of Fox News.

There is nothing wrong with grabbing a rate in the 5% range right now, especially if it gives you payments you can afford. My gosh, that's better than a 3.5 point difference. So in your case, the second time could be a charm.

If you are not successful, check out www.makinghomeaffordable.gov, which outlines the administration's plan to help stabilize the housing market by reducing the mortgage payments of up to 9 million eligible homeowners.

The refinance portion of the effort gives up to 5 million owners with loans owned or guaranteed by either Fannie Mae or Freddie Mac an opportunity to trade in their loans for ones that are easier on their pocketbooks. And the loan modification part commits $75 billion to keep as many as 4 million other families in their homes by preventing avoidable foreclosure.

The Web site has detailed information about these programs along with self-assessment tools and calculators to empower borrowers with the resources they need to determine whether they might be eligible for a modification or a refinance under the program. Check out the Making Home Affordable site.

Borrowers also can use the site to connect to free counseling resources to answer any questions they may have about their own personal situations. You'll also find a checklist of key documents and materials to have ready when making that important call to your lender as well as FAQs from borrowers in similar circumstances.

Q: I enjoyed your article on tax credits for energy efficient home improvements. The question I have is, do the credits phase out at higher income levels like so many of the recent tax rebates and credits (typically over $75,000).

A: Good news. There are no income limitations on the energy credits. So feel free to spend away.

Q: Great article on reverse mortgage for seniors who want to scale down the housing ladder. What happens to the lower property tax basis on the first house, the one in California? Who pays the property tax bill, and could they have used the lower or carryover basis of the old property tax basis since they over 55? See previous Realty Q&A.

A: I'm an East Coast guy who doesn't know all that much about the Left Coast. So I turned your question over to Robert D. Yeary, CEO of Reverse Mortgage Solutions. The Spring, Tex., firm has developed a specialized, state of the art system to service reverse mortgages in all jurisdictions. Here's his response:

"In California, you can transfer your old tax base to a new house, provided the county in which you purchase your new home allows that transfer. Not all counties do that. But even in jurisdictions that do allow a transfer, if you pay more for the new house, you can only transfer the tax base if the purchase price is no greater than 105% of the amount for which you sold your previous residence. If you wait a full year after the sale of your home, you can transfer 110% of the selling price."

If the new house is considerably less expensive that the home you sold, Yeary suggests considering what the property tax would be without transferring the lower basis to the new place.

"Surprisingly," he says, "in California, real estate taxes are fairly low thanks to Proposition 13. Taxes are set at the time you purchase the home and can go up only so much every year. There are plenty of houses worth $500,000 or more in California with low tax bases because they were purchased years ago for $35,000."

Yeary also notes that the Golden State offers several tax relief program for low and moderate-income seniors.

Source

May 10, 2009

Where can working Americans afford a home?

They are still priced out of the housing market in many cities across the country, a new study concludes.

Housing prices may have plummeted, but they’re still not affordable for many working men and women in America.

The National Housing Conference Thursday released its annual “Paycheck to Paycheck” report, which compares workers salaries and home prices in more than 200 communities across the country.

The bursting of the real estate bubble has made owning a home more affordable for some, with the median price of a home dropping 14.5 percent nationally in the past year, the report concluded. But the majority of essential workers like teachers, police, and firefighters still cannot afford to buy a home in the towns and cities where they work, it added.

The “Paycheck to Paycheck” report takes an in-depth look at construction-related jobs, which are expected to get a boost from the Obama administration’s stimulus package. It analyzed five jobs: construction managers, carpenters, equipment operators, long-haul truck drivers, and construction laborers. It concluded that only construction managers, who make about $100,000 a year, can afford to buy a home in the 208 housing markets analyzed.

Carpenters were able to afford to own a home in 51 of the 208 studied markets, and equipment operators in 35 markets. Construction laborers were priced out of 196 of the communities.

“Just because prices are falling, that doesn’t mean that we have seen an end to the problem of affordability, because for many people, particularly at the low end of the income spectrum, people are losing their jobs or their hours are being cut back,” says Nicolas Retsinas, director of Harvard’s Joint Center on Housing Studies.

“So it’s not just the cost of housing, whether to purchase or rent, but it is also people’s ability to pay,” he adds. “And in this economic situation we’re in, that’s becoming much more problematic.”

San Francisco remains the most expensive city in which to buy a home, with a median price of $575,000, according to the report. That’s down from $770,000 a year ago. New York ranks second with a median price of $455,000, a drop of $70,000 from a year ago. The least expensive places are Saginaw, Mich., and Youngstown, Ohio, each with a median home price of $73,000.

That price is affordable for most working Americans. But there’s a catch. “The problem in a lot of these more-affordable areas is that unemployment is a substantial problem, so being able to actually purchase a home still may not be in everyone’s cards,” says Maya Brennan, a researcher at the Center for Housing Policy, the research arm of the National Housing Conference.

The report also found that rents rose nationally by 3.7 percent in the past year. But in Florida, which has been hit hard by the foreclosure crisis, rents spiked more significantly.

“One hypothesis is that as people are losing their homes, they become renters. And in the past renters could easily become homeowners, but now that door is shut to many,” says Professor Retsinas. “So in some markets, you see an increase in demand for rental housing, and an increase in demand for anything has a tendency to raise prices.”

The data have prompted calls for federal, state, and local officials to create more affordable housing, particularly in high-priced urban areas. The Department of Housing and Urban Development already has a Neighborhood Stabilization Program, which is designed to rehabilitate abandoned foreclosed homes, a certain amount of which must be affordable. But housing experts say that much more needs to be done.

“Although home prices have dropped, states and localities and the nation as a whole still have to pay attention to the needs of low- and moderate-income workers,” says Ms. Brennan. “A lot of communities can take advantage of the lower home prices to try to buy some properties themselves and get them preserved as affordable housing for the future.”

Some housing policy experts like Retinas see the housing market crisis as an opportunity.

“There’s an irony that in the midst of this calamity in the housing market, there’s a reaffirmation of the adage that housing really matters,” he says. “It was very difficult in years gone by to put affordable housing on the agenda, because people considered it an afterthought. Now have learned full well what happens when people lose their homes and are unable to afford a place to live.”

Source

Housing prices may have plummeted, but they’re still not affordable for many working men and women in America.

The National Housing Conference Thursday released its annual “Paycheck to Paycheck” report, which compares workers salaries and home prices in more than 200 communities across the country.

The bursting of the real estate bubble has made owning a home more affordable for some, with the median price of a home dropping 14.5 percent nationally in the past year, the report concluded. But the majority of essential workers like teachers, police, and firefighters still cannot afford to buy a home in the towns and cities where they work, it added.

The “Paycheck to Paycheck” report takes an in-depth look at construction-related jobs, which are expected to get a boost from the Obama administration’s stimulus package. It analyzed five jobs: construction managers, carpenters, equipment operators, long-haul truck drivers, and construction laborers. It concluded that only construction managers, who make about $100,000 a year, can afford to buy a home in the 208 housing markets analyzed.

Carpenters were able to afford to own a home in 51 of the 208 studied markets, and equipment operators in 35 markets. Construction laborers were priced out of 196 of the communities.

“Just because prices are falling, that doesn’t mean that we have seen an end to the problem of affordability, because for many people, particularly at the low end of the income spectrum, people are losing their jobs or their hours are being cut back,” says Nicolas Retsinas, director of Harvard’s Joint Center on Housing Studies.

“So it’s not just the cost of housing, whether to purchase or rent, but it is also people’s ability to pay,” he adds. “And in this economic situation we’re in, that’s becoming much more problematic.”

San Francisco remains the most expensive city in which to buy a home, with a median price of $575,000, according to the report. That’s down from $770,000 a year ago. New York ranks second with a median price of $455,000, a drop of $70,000 from a year ago. The least expensive places are Saginaw, Mich., and Youngstown, Ohio, each with a median home price of $73,000.

That price is affordable for most working Americans. But there’s a catch. “The problem in a lot of these more-affordable areas is that unemployment is a substantial problem, so being able to actually purchase a home still may not be in everyone’s cards,” says Maya Brennan, a researcher at the Center for Housing Policy, the research arm of the National Housing Conference.

The report also found that rents rose nationally by 3.7 percent in the past year. But in Florida, which has been hit hard by the foreclosure crisis, rents spiked more significantly.

“One hypothesis is that as people are losing their homes, they become renters. And in the past renters could easily become homeowners, but now that door is shut to many,” says Professor Retsinas. “So in some markets, you see an increase in demand for rental housing, and an increase in demand for anything has a tendency to raise prices.”

The data have prompted calls for federal, state, and local officials to create more affordable housing, particularly in high-priced urban areas. The Department of Housing and Urban Development already has a Neighborhood Stabilization Program, which is designed to rehabilitate abandoned foreclosed homes, a certain amount of which must be affordable. But housing experts say that much more needs to be done.

“Although home prices have dropped, states and localities and the nation as a whole still have to pay attention to the needs of low- and moderate-income workers,” says Ms. Brennan. “A lot of communities can take advantage of the lower home prices to try to buy some properties themselves and get them preserved as affordable housing for the future.”

Some housing policy experts like Retinas see the housing market crisis as an opportunity.

“There’s an irony that in the midst of this calamity in the housing market, there’s a reaffirmation of the adage that housing really matters,” he says. “It was very difficult in years gone by to put affordable housing on the agenda, because people considered it an afterthought. Now have learned full well what happens when people lose their homes and are unable to afford a place to live.”

Source

May 9, 2009

First 100 days of Obama: Stimulus plan includes tax breaks for many people

Whether the multibillion-dollar economic stimulus plan will actually jump-start the nation's ailing economy is uncertain.

But one thing is for sure: The plan has real perks for many American families -- some worth hundreds of dollars, some worth thousands. Of course, some families will benefit little, if at all.

For more information on the incentives, go to www.irs.gov and click on "Update on Recovery Tax Provisions for Individuals and Businesses."

Break for home buyers » Buy a home before Dec. 1 and you could get as much as $8,000.

The money is a tax credit that does not have to be repaid if the home remains your primary residence for at least three years. Although it is touted as an incentive for first-time buyers, those who have owned homes in the past may qualify, as well.

The IRS defines a first-time buyer as someone who has not owned a home in the three years prior to the date he or she closes on a home this year.

The free money is available only to those who have purchased after Jan. 1. Buyers who purchased between April 8 and Dec. 31, 2008, are eligible for an incentive worth as much as $7,500, but that must be repaid.

The credit is reduced or eliminated for higher-income taxpayers. It begins to be phased out for single filers with modified adjusted gross incomes of more than $75,000. Those earning more than $95,000 don't qualify.

Advertisement

For married couples filing jointly, the credit begins to be phased out at incomes of more than $150,000; those earning more than $170,000 don't qualify.

Incentive for car buyers » Purchase a new car, light truck, motor home or motorcycle and you may be entitled to deduct the taxes you paid on next year's tax return.

Taxes on up to $49,500 of the purchase price may be deducted if you bought after Feb. 16 and before Jan. 1, 2010.

Unlike the homebuyer tax credit, which reduces your tax liability dollar for dollar, this deduction simply reduces your taxable income. So, its value depends on your tax bracket.

The amount of this deduction also is phased out for higher-income taxpayers. Don't itemize? That doesn't matter -- you can still take this deduction.

In addition to the $8,000 federal incentive, Utah is offering $6,000 grants to homebuyers. Unlike the federal money, the state incentive is available only for those who buy new homes, and it's limited to the first 1,600 home buyers. About 1,100 grants are still available. For information, go to www.utahhousingcorp.org.

More money in worker paychecks » Most taxpayers qualify for a tax credit of up to $400 this year and next -- $800 for married couples filing jointly.

But taxpayers won't have to wait until they file their returns before they get their money. This benefit is being coordinated with employers, who are delivering the incentive by withholding less money from paychecks -- to the tune of about $45 to $65 more per month for some people.

The credit, based on 6.2 percent of earned income, phases out for higher-income taxpayers.

To compensate for the reduced amount being withheld, employees will take a tax credit when filing 2009 and 2010 returns. So, even though less money is being taken out of paychecks, employees won't owe more in taxes or get less of a refund.

More benefits for the unemployed » Weekly unemployment benefits have been increased by $25 per week, and workers who exhaust 26 weeks of unemployment benefits may be eligible for 20 additional weeks.

Even better, the first $2,400 of unemployment benefits a person receives in 2009 is tax free. Additionally, many laid-off workers are eligible for a new 65 percent subsidy that helps cover much of the high cost of continuing health insurance coverage under the federal COBRA program.

The subsidy is available for up to nine months. You must have been laid off between Sept. 1, 2008, and Dec. 31 of this year to qualify. For information, call your former employer's human resources department or contact the Utah Department of Insurance at www.insurance.utah.gov or by calling (801) 538-3077.

Source

But one thing is for sure: The plan has real perks for many American families -- some worth hundreds of dollars, some worth thousands. Of course, some families will benefit little, if at all.

For more information on the incentives, go to www.irs.gov and click on "Update on Recovery Tax Provisions for Individuals and Businesses."

Break for home buyers » Buy a home before Dec. 1 and you could get as much as $8,000.

The money is a tax credit that does not have to be repaid if the home remains your primary residence for at least three years. Although it is touted as an incentive for first-time buyers, those who have owned homes in the past may qualify, as well.

The IRS defines a first-time buyer as someone who has not owned a home in the three years prior to the date he or she closes on a home this year.

The free money is available only to those who have purchased after Jan. 1. Buyers who purchased between April 8 and Dec. 31, 2008, are eligible for an incentive worth as much as $7,500, but that must be repaid.

The credit is reduced or eliminated for higher-income taxpayers. It begins to be phased out for single filers with modified adjusted gross incomes of more than $75,000. Those earning more than $95,000 don't qualify.

Advertisement

For married couples filing jointly, the credit begins to be phased out at incomes of more than $150,000; those earning more than $170,000 don't qualify.

Incentive for car buyers » Purchase a new car, light truck, motor home or motorcycle and you may be entitled to deduct the taxes you paid on next year's tax return.

Taxes on up to $49,500 of the purchase price may be deducted if you bought after Feb. 16 and before Jan. 1, 2010.

Unlike the homebuyer tax credit, which reduces your tax liability dollar for dollar, this deduction simply reduces your taxable income. So, its value depends on your tax bracket.

The amount of this deduction also is phased out for higher-income taxpayers. Don't itemize? That doesn't matter -- you can still take this deduction.

In addition to the $8,000 federal incentive, Utah is offering $6,000 grants to homebuyers. Unlike the federal money, the state incentive is available only for those who buy new homes, and it's limited to the first 1,600 home buyers. About 1,100 grants are still available. For information, go to www.utahhousingcorp.org.

More money in worker paychecks » Most taxpayers qualify for a tax credit of up to $400 this year and next -- $800 for married couples filing jointly.

But taxpayers won't have to wait until they file their returns before they get their money. This benefit is being coordinated with employers, who are delivering the incentive by withholding less money from paychecks -- to the tune of about $45 to $65 more per month for some people.

The credit, based on 6.2 percent of earned income, phases out for higher-income taxpayers.

To compensate for the reduced amount being withheld, employees will take a tax credit when filing 2009 and 2010 returns. So, even though less money is being taken out of paychecks, employees won't owe more in taxes or get less of a refund.

More benefits for the unemployed » Weekly unemployment benefits have been increased by $25 per week, and workers who exhaust 26 weeks of unemployment benefits may be eligible for 20 additional weeks.

Even better, the first $2,400 of unemployment benefits a person receives in 2009 is tax free. Additionally, many laid-off workers are eligible for a new 65 percent subsidy that helps cover much of the high cost of continuing health insurance coverage under the federal COBRA program.

The subsidy is available for up to nine months. You must have been laid off between Sept. 1, 2008, and Dec. 31 of this year to qualify. For information, call your former employer's human resources department or contact the Utah Department of Insurance at www.insurance.utah.gov or by calling (801) 538-3077.

Source

May 8, 2009

First-time homebuyer? Take advantage of this tax benefit

Under two recent pieces of federal legislation, a first-time homebuyer may be able to take advantage of a tax benefit when purchasing a home.

Note that a "first time home buyer" includes those who have not owned a home in the three years prior to a current purchase, but may have owned a home prior to those three years.

For married taxpayers, the law tests the homeownership history of both the home buyer and his/her spouse. But there are two different types of credits: one for those who purchased a home between April 9, 2008, and Dec. 31, 2008, who may be eligible for a federal tax credit of up to $7,500, and another for first-time buyers who purchase a home between Jan. 1, 2009, and before Dec. 1, 2009, who may be eligible for a federal tax credit of up to $8,000.

In either case, the credit is equal to 10 percent of the purchase price of a principal residence, up to $7,500 or $8,000.

There are, however, differing effects to the two credits. Unlike other types of tax credits, the first-time homebuyer credit for 2008 must be repaid over 15 years. Furthermore, it will need to be repaid in full if the taxpayer sells the house within the 16-year repayment period.

Some have described the credit as an "interest-free loan" because of this repayment requirement.

In contrast, the 2009 tax credit does not have to be repaid, but home buyers must use the residence as a principal residence for at least three years, or face recapture of the tax credit amount.

The credit is phased out, or reduced, for individuals with modified adjusted gross income between $75,000 and $95,000. For married couples filing a joint return, the phase out range is $150,000 to $170,000.

The tax credit amount is reduced to zero for taxpayers with adjusted gross income of more than $95,000 (single) or $170,000 (married), and is reduced proportionally for taxpayers with adjusted gross income between these amounts.

To determine modified adjusted gross income, it is necessary to add certain sums, such as foreign income, foreign-housing deductions, student-loan deductions, IRA contribution deductions and deductions for higher-education costs.

Interestingly, the credit is fully refundable, meaning taxpayers will be able to obtain an additional federal tax refund of up to $7,500 or $8,000, even if they have no other tax liabilities or if the credit is more than the tax that they owe. Typically this involves the government sending the taxpayer a check for a portion, or even all, of the amount of the refundable tax credit.

For a home that a taxpayer builds, the purchase date is the first date of occupancy of the home. For a pre-existing home, the purchase date is the date when closing occurs and the title to the property transfers to the home owner.

A primary residence is a residence in which an individual lives most of the time and can be a house, condominium, or even mobile home. The definition of principal residence is identical to the one used to determine whether you may qualify for the $250,000-$500,000 capital gain tax exclusion for principal residences.

People who purchased a home between April 9, 2008, and Dec. 31, 2008, (the $7,500 credit) should claim the credit on their 2008 tax returns, and may need to amend the return if one has already been filed. The credit must be repaid in 15 equal installments over 15 years, beginning with the 2010 tax year.

People who purchased a home between Jan. 1, 2009, and before Dec. 1, 2009, (the $8,000 credit), can claim the credit on their 2008 or 2009 tax returns (if the 2008 return is already filed, the taxpayer will need to amend that return to treat the purchase as occurring on Dec. 31, 2008).

Taxpayers using the 2009 credit do not have to repay it provided the home remains their main residence for 36 months after the purchase date.

Given the complexities with the differing credits, and the fact that an amended tax return may need to be filed, readers are urged to consult with their financial, tax and legal professionals to assist in claiming the refund.

Source

Note that a "first time home buyer" includes those who have not owned a home in the three years prior to a current purchase, but may have owned a home prior to those three years.

For married taxpayers, the law tests the homeownership history of both the home buyer and his/her spouse. But there are two different types of credits: one for those who purchased a home between April 9, 2008, and Dec. 31, 2008, who may be eligible for a federal tax credit of up to $7,500, and another for first-time buyers who purchase a home between Jan. 1, 2009, and before Dec. 1, 2009, who may be eligible for a federal tax credit of up to $8,000.

In either case, the credit is equal to 10 percent of the purchase price of a principal residence, up to $7,500 or $8,000.

There are, however, differing effects to the two credits. Unlike other types of tax credits, the first-time homebuyer credit for 2008 must be repaid over 15 years. Furthermore, it will need to be repaid in full if the taxpayer sells the house within the 16-year repayment period.

Some have described the credit as an "interest-free loan" because of this repayment requirement.

In contrast, the 2009 tax credit does not have to be repaid, but home buyers must use the residence as a principal residence for at least three years, or face recapture of the tax credit amount.

The credit is phased out, or reduced, for individuals with modified adjusted gross income between $75,000 and $95,000. For married couples filing a joint return, the phase out range is $150,000 to $170,000.

The tax credit amount is reduced to zero for taxpayers with adjusted gross income of more than $95,000 (single) or $170,000 (married), and is reduced proportionally for taxpayers with adjusted gross income between these amounts.

To determine modified adjusted gross income, it is necessary to add certain sums, such as foreign income, foreign-housing deductions, student-loan deductions, IRA contribution deductions and deductions for higher-education costs.

Interestingly, the credit is fully refundable, meaning taxpayers will be able to obtain an additional federal tax refund of up to $7,500 or $8,000, even if they have no other tax liabilities or if the credit is more than the tax that they owe. Typically this involves the government sending the taxpayer a check for a portion, or even all, of the amount of the refundable tax credit.

For a home that a taxpayer builds, the purchase date is the first date of occupancy of the home. For a pre-existing home, the purchase date is the date when closing occurs and the title to the property transfers to the home owner.

A primary residence is a residence in which an individual lives most of the time and can be a house, condominium, or even mobile home. The definition of principal residence is identical to the one used to determine whether you may qualify for the $250,000-$500,000 capital gain tax exclusion for principal residences.

People who purchased a home between April 9, 2008, and Dec. 31, 2008, (the $7,500 credit) should claim the credit on their 2008 tax returns, and may need to amend the return if one has already been filed. The credit must be repaid in 15 equal installments over 15 years, beginning with the 2010 tax year.

People who purchased a home between Jan. 1, 2009, and before Dec. 1, 2009, (the $8,000 credit), can claim the credit on their 2008 or 2009 tax returns (if the 2008 return is already filed, the taxpayer will need to amend that return to treat the purchase as occurring on Dec. 31, 2008).

Taxpayers using the 2009 credit do not have to repay it provided the home remains their main residence for 36 months after the purchase date.

Given the complexities with the differing credits, and the fact that an amended tax return may need to be filed, readers are urged to consult with their financial, tax and legal professionals to assist in claiming the refund.

Source

May 7, 2009

New tax credit available for homebuyers

Missouri is offering a unique addition to a federal tax credit program intended to bring the country's housing market out of the doldrums by offering credits to first-time homebuyers.

The program, which is part of the $787 billion federal stimulus package passed in February, increases the amount that first-time homebuyers can receive from the program from $7,500 to $8,000. The original amount was set in stimulus package passed in November 2008.

The Missouri Housing and Development Commission is offering a variation of the program that no other U.S. state is practicing. The commission is offering to preemptively loan homebuyers the money for the federal tax credit before the federal government distributes the credit. The homebuyer then turns federal credit over to the state commission, and must keep the same address for three years. The homebuyer must also pay back the loan before June 2010 to avoid interest charges.

Without this variation, homebuyers in Missouri would first have to purchase a home, and then would receive their tax credit after they filed their income taxes for the following tax season.

U.S. Sen. Claire McCaskill, D-Mo., was in Columbia on Saturday for a news conference to discuss the program. The conference was held at the home of Travis and Jessica Peterson, two longtime Columbia residents who just purchased a home on the east side of the city and soon thereafter received $8,000 from the program.

In a news release issued prior to her appearance, McCaskill said the tax credit program would help to recover the economy.

"Buying a first home is an integral part of the American dream and the economic recovery package gives first-time homebuyers a tremendous incentive and help in realizing that dream," McCaskill said in the release.

The Petersons, who had already purchased the house but received the credit, said they were going to use the money to build a privacy fence around the backyard of the house.

Jessica Peterson said the fence would be useful because the couple is expecting a child in October.

"We're very happy he could do this," Peterson said.

Columbia Board of Realtors President Carol Van Gorp said since the beginning of March, 14 percent of homes sold in Columbia used the tax credit.

Van Gorp said the credit could be useful for college-aged homebuyers that seek to leave rental properties. She said it was not uncommon for the parents of students to buy houses in the names of their children so that they can cash in on the credit.

Van Gorp said the program would help stimulate the economy, not only by moving sluggish housing sales, but also through the purchase of consumer goods and the collection of sales tax.

"We need housing to recover so that the economy can recover," Van Gorp said.

According to data released by the Kaiser Family Foundation, the rate of foreclosures in Missouri was lower than the national average. According to the National Association of Home Builders, there was an increase in new home sales in the U.S. in March, up almost 20,000 new homes from 331,000 sold in January. In March 2008, though, 513,000 homes were sold in the U.S.

Andi Benson, a spokeswoman for the Missouri Housing and Development Commission, said 97 home sales have closed using the credit, and an additional 257 are being processed. She said 47 of the cleared sales went to owners in their 20s.

Benson said the loan was intended to help first time homebuyers pay their down payments and closing costs.

"Most of us don't have that kind of money laying around," Benson said.

Source

The program, which is part of the $787 billion federal stimulus package passed in February, increases the amount that first-time homebuyers can receive from the program from $7,500 to $8,000. The original amount was set in stimulus package passed in November 2008.

The Missouri Housing and Development Commission is offering a variation of the program that no other U.S. state is practicing. The commission is offering to preemptively loan homebuyers the money for the federal tax credit before the federal government distributes the credit. The homebuyer then turns federal credit over to the state commission, and must keep the same address for three years. The homebuyer must also pay back the loan before June 2010 to avoid interest charges.

Without this variation, homebuyers in Missouri would first have to purchase a home, and then would receive their tax credit after they filed their income taxes for the following tax season.

U.S. Sen. Claire McCaskill, D-Mo., was in Columbia on Saturday for a news conference to discuss the program. The conference was held at the home of Travis and Jessica Peterson, two longtime Columbia residents who just purchased a home on the east side of the city and soon thereafter received $8,000 from the program.

In a news release issued prior to her appearance, McCaskill said the tax credit program would help to recover the economy.

"Buying a first home is an integral part of the American dream and the economic recovery package gives first-time homebuyers a tremendous incentive and help in realizing that dream," McCaskill said in the release.

The Petersons, who had already purchased the house but received the credit, said they were going to use the money to build a privacy fence around the backyard of the house.

Jessica Peterson said the fence would be useful because the couple is expecting a child in October.

"We're very happy he could do this," Peterson said.

Columbia Board of Realtors President Carol Van Gorp said since the beginning of March, 14 percent of homes sold in Columbia used the tax credit.

Van Gorp said the credit could be useful for college-aged homebuyers that seek to leave rental properties. She said it was not uncommon for the parents of students to buy houses in the names of their children so that they can cash in on the credit.

Van Gorp said the program would help stimulate the economy, not only by moving sluggish housing sales, but also through the purchase of consumer goods and the collection of sales tax.

"We need housing to recover so that the economy can recover," Van Gorp said.

According to data released by the Kaiser Family Foundation, the rate of foreclosures in Missouri was lower than the national average. According to the National Association of Home Builders, there was an increase in new home sales in the U.S. in March, up almost 20,000 new homes from 331,000 sold in January. In March 2008, though, 513,000 homes were sold in the U.S.

Andi Benson, a spokeswoman for the Missouri Housing and Development Commission, said 97 home sales have closed using the credit, and an additional 257 are being processed. She said 47 of the cleared sales went to owners in their 20s.

Benson said the loan was intended to help first time homebuyers pay their down payments and closing costs.

"Most of us don't have that kind of money laying around," Benson said.

Source

May 6, 2009

Home Prices Still Dropping - Just Not as Fast

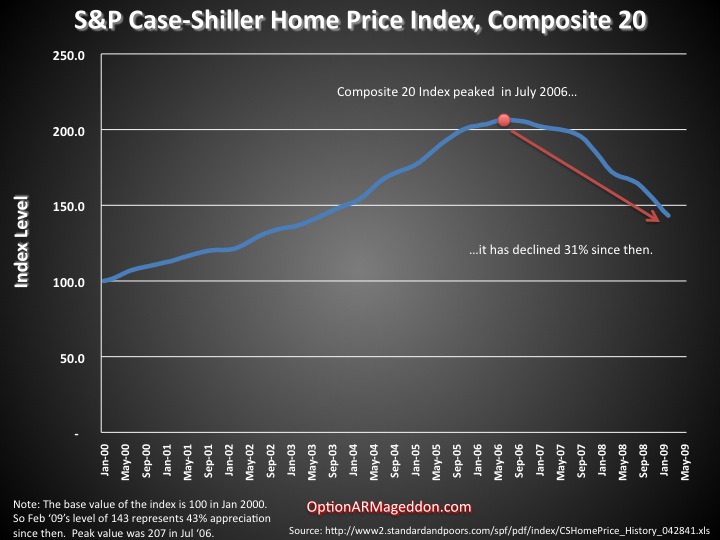

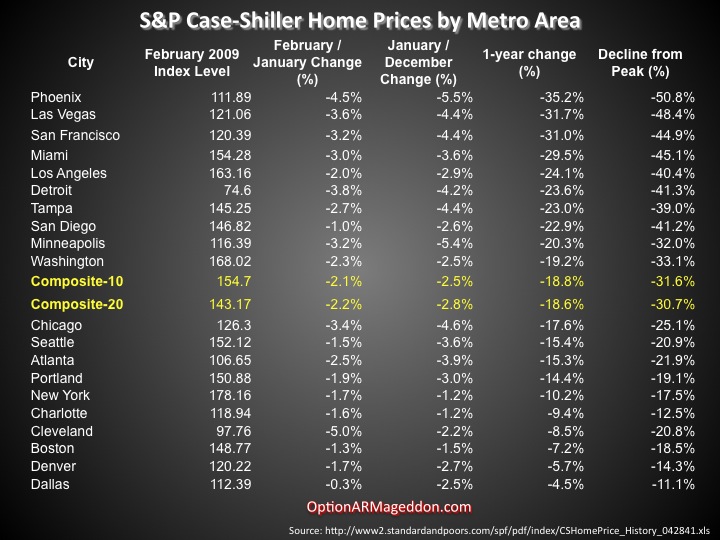

February Data for the S&P Case-Shiller Index was released today. Prices are still falling, and quickly. Each of the 20 major metro areas measured by the index showed another a month-over-month decline, for the fifth month in a row. The Composite 20 Index is now off 31% from its peak, reached in July 2006. It fell another 2.2% from January to February. 15 of the 20 metro areas showed a greater than 10% fall in prices versus last year and one city, Phoenix, has now fallen over 50% from its peak. (More detail by metro area in the table below.)

Despite the government’s efforts to put a floor under house prices—printing money to buy MBS in order to hold down interest rates, acting as lender of last resort via Fannie/Freddie/FHA—prices continue to fall. This is bad news for bank balance sheets and existing homeowners, but good news (sort of) for the rest of us who’d like to purchase a home one day at a reasonable cost. Unfortunately, as home prices continue to fall, even renters are put at risk. Everyone who keeps their savings in banks and/or is employed by someone that does, is put at risk as the collateral supporting bank balance sheets continues to deteriorate. Even prime borrowers are defaulting in much greater numbers as house prices fall. This is because negative equity is a better predictor of default than a borrower’s credit rating.

Incidentally, there are those who argue now is the time to buy since interest rates are so low and house prices have declined. I disagree. If you’re planning to live in the house for many years, you have to consider that mortgage rates are likely to increase while you’re still in the house. If incomes don’t increase as well, then the monthly payment an average buyer will be able to afford will stay the same. Same monthly payment + higher interest rates = lower home values.

In other words, with higher rates, the interest component of the monthly payment will be higher. To compensate, house prices will have to fall farther. Higher incomes could support higher house prices, but my feeling is interest rates are likely to head higher before incomes do.

This gets us back to the cheap credit “trap” being set by the Fed. It can’t raise rates, even when the economy returns to “normal.” If it does it will blow a bigger hole in bank balance sheets as the values of interest-rate sensitive assets decline.

Getting back to the data, I’ve added a column at right that shows the decline from the peak for each metro area. The Comp 20 peak was reached in July 2006, but individual metro areas peaked at different times. Boston, for instance, peaked in September 2005 while Charlotte peaked in August 2007.

Source

Despite the government’s efforts to put a floor under house prices—printing money to buy MBS in order to hold down interest rates, acting as lender of last resort via Fannie/Freddie/FHA—prices continue to fall. This is bad news for bank balance sheets and existing homeowners, but good news (sort of) for the rest of us who’d like to purchase a home one day at a reasonable cost. Unfortunately, as home prices continue to fall, even renters are put at risk. Everyone who keeps their savings in banks and/or is employed by someone that does, is put at risk as the collateral supporting bank balance sheets continues to deteriorate. Even prime borrowers are defaulting in much greater numbers as house prices fall. This is because negative equity is a better predictor of default than a borrower’s credit rating.

Incidentally, there are those who argue now is the time to buy since interest rates are so low and house prices have declined. I disagree. If you’re planning to live in the house for many years, you have to consider that mortgage rates are likely to increase while you’re still in the house. If incomes don’t increase as well, then the monthly payment an average buyer will be able to afford will stay the same. Same monthly payment + higher interest rates = lower home values.

In other words, with higher rates, the interest component of the monthly payment will be higher. To compensate, house prices will have to fall farther. Higher incomes could support higher house prices, but my feeling is interest rates are likely to head higher before incomes do.

This gets us back to the cheap credit “trap” being set by the Fed. It can’t raise rates, even when the economy returns to “normal.” If it does it will blow a bigger hole in bank balance sheets as the values of interest-rate sensitive assets decline.

Getting back to the data, I’ve added a column at right that shows the decline from the peak for each metro area. The Comp 20 peak was reached in July 2006, but individual metro areas peaked at different times. Boston, for instance, peaked in September 2005 while Charlotte peaked in August 2007.

Source

Subscribe to:

Posts (Atom)