As a way to help seniors looking to either downsize their homes or purchase a new home, MLS Reverse Mortgage has begun offering reverse mortgages for home purchase. Now seniors can purchase a home with no monthly payments.

On January 1, 2009, HUD/FHA began insuring reverse mortgages used to purchase homes. In the past, reverse mortgages have only been available as a refinance loan to seniors who already resided in the home.

This is fantastic news for senior homeowners aged 62 and older. But, what does it really mean to seniors? Well, it gives seniors the opportunity to purchase a new home without monthly payments. Reverse mortgages do not have credit or income requirements, therefore, this will make buying a home for first time buyers, seniors looking to downsize from their existing homes or those seniors needing special requirements like wider hallways, much easier to obtain. Reverse mortgages are based on appraised value and Borrowers age. As a rule of thumb, the older you are, the more you qualify for.

"I'm ecstatic to be able to offer the reverse mortgage for home purchase," stated Mike Borba, President of Borba Investments, Inc. dba MLS Reverse Mortgage. "I feel it's truly a needed product and will help hundreds of seniors more comfortably age in place."

For those interested in the purchase reverse mortgage, a quick phone call to MLS Reverse Mortgage will answer a lot of burning questions. For example, how much money will I need as a down payment? Also, if you know how much money you have available for down payment, MLS Reverse Mortgage can let you know the purchase price range of homes that you should be looking for.

Example 1: A 65-year-old borrower who purchases a $300,000 house would need about $125,000 to put into the transaction as a down payment and towards closing costs. *

Example 2: A 65-year-old borrower has $65,000 to use as a down payment and towards closing costs. She/He would qualify to purchase a home valued around $144,000. *

Reverse Mortgages have seen a major jump in popularity over the past few years. But, what is a Reverse Mortgage? A majority of senior homeowners would like to stay in their own homes throughout their retirement years. However, everything from rising healthcare costs to increasing home maintenance expenses are making that more and more difficult. As a response to the apparent problem, the U.S. government created a financial solution for homeowners 62 and older. The solution is called a Reverse Mortgage and it may just help seniors truly enjoy their retirement years. A reverse mortgage enables homeowners 62 or older to convert part of the equity in their homes into tax-free income without having to sell their home, give up title, or take on a new monthly mortgage payment. And now, seniors have the option to use a reverse mortgage to purchase a new home.

Source

February 24, 2009

February 23, 2009

Southern California home prices fall to 2002 levels

A home for sale in Altadena. As values slide, Southern California may be at the start of a long period of relatively affordable housing.

January's median sales price falls 40% from a year earlier, to $250,000. As the Southland's bubble continues to deflate, the ratio of price to income has returned to normal, analysts say.

By Peter Y. Hong

February 20, 2009

Southern California -- with home prices now at 2002 levels and falling -- is at the start of what is likely to be a long period of relatively affordable housing, economists and housing market analysts say.

Home prices are now below their historical average compared with incomes, putting them within reach of more people than they have been since about 2000, several studies show.

But that doesn't mean prices will stop falling soon, especially if jobs continue to vanish at their current pace.

After soaring during this decade's housing bubble, home prices recently fell back in line with what people earn -- and then kept falling.

The January median sales price for Southern California homes fell to $250,000, a 40% drop from the same month a year prior, the San Diego real estate research firm MDA DataQuick reported Thursday. The price decline was accelerated by foreclosures, which accounted for 60% of sales last month.

Prices have now dipped below the level at which they'd be in line with the historical ratio of prices to incomes in California, said Christopher Thornberg, a Los Angeles economist who is principal of the consulting firm Beacon Economics.

Thornberg estimates the current median home value in California is $250,000. But wages are high enough -- and interest rates low enough -- that a median value of $290,000 would match historical norms, he said.

"If you're looking for a long-run opportunity, real estate is getting to that point," said Thornberg, who was an early predictor of the housing crash.

But it's not at that point yet.

Thornberg believes home prices have another 25% to 30% to drop. They may be historically low, but "in the past four or five months, unemployment has been through the roof," Thornberg said.

Fearing for their jobs, many potential home buyers are putting off a purchase. Others simply can't buy anything because they are already out of work.

Thornberg forecasts that California home prices will fall until the middle of 2010, when they will begin to slowly creep up.

The local housing market is now in what economists call the "overshoot" stage, when a mid-priced home sells for less than it typically would based on median incomes. Even though homes become relatively affordable, the real estate market tends to linger for years at below-average prices as joblessness persists or buyers shy away.

John Burns, an Irvine consultant to home builders, said he expected the market to continue to drop despite the increase in affordability.

"They're still not as affordable as they were in 1995 and 1996, and I think there's an almost certainty prices will keep falling," Burns said.

Even after the economy exits the recession, people will continue to lack the confidence to buy a home, Burns said. "It's bubble psychology. People believe when something happens for three, four or five years in a row, it's likely to keep happening. It happens in boom times as well."

Burns predicts home prices in the Los Angeles area won't rise again until 2012.

An analysis by Burns shows that the last time Los Angeles home prices dropped below their historical average relative to incomes, in 1992, they kept falling until 1997 and didn't return to their 1992 level relative to incomes until 2002.

In a downturn, prices also tend to fall relatively slowly in more affluent areas. Homeowners there are less likely to be threatened by foreclosure and can delay selling their homes.

The number of January home sales in Bel-Air, Beverly Hills, Santa Monica, Laguna Beach and Newport Beach were all below average or at record lows, DataQuick reported, noting that "such areas have so far seen relatively small price declines and haven't benefited from the wave of bargain hunting that's boosted inland sales for months."

That's why Aarchan Joshi, a 40-year-old ophthalmologist who lives in north Redondo Beach, is putting off a move to Manhattan Beach. He could afford to move now but thinks "there's a big disconnect. The more affluent areas are really just beginning" their price declines, he said. read more

February 22, 2009

An unusual incentive to buy a home

Charlotte homebuilder offers partial refund if area home values fall more than 10% within a year of purchase.

Ray Killian Jr., CEO and Director of Simonini Builders of Charlotte.

Ray Killian Jr., CEO and Director of Simonini Builders of Charlotte.

One reason houses aren't selling is that people are worried prices will drop further.

A Charlotte homebuilder is offering an unusual incentive to help offset that concern.

Simonini Builders will refund customers up to 5 percent of what they paid for a house if Charlotte-area home values take a steep plunge. The refund kicks in if values decline within a year of purchase by more than 10 percent and up to 15 percent, based on a widely used home price index.

On a $700,000 house, the refund would be $700 for a decline of 10.1 percent, to as much as $35,000 if values fall 15 percent.

“We view it more as an insurance policy for the consumer,” said Ray Killian Jr., CEO and co-owner of the company. “We give them a hedge.”

For more than a year, new home construction has been plunging locally and nationwide as lending standards tightened, foreclosures glutted the market, unemployment rose and the economy soured. Even people with good credit and relatively secure jobs are hesitant to spend. And the ongoing decline in home values has some buyers holding out for lower prices or unwilling to buy and risk a quick loss.

Discounting and other incentives have been common among builders hungry for sales. Killian says they've already cut prices 8 percent to 13 percent.

But several real estate experts said they hadn't heard of a refund plan like the Simonini deal. The hedge, which Killian credits to Chief Financial Officer Bill Saint, is based on the widely watched S&P/Case-Shiller Home Price Index.

“It's a very clever idea,” said François Ortalo-Magné, a professor and chairman of the real estate department at the University of Wisconsin-Madison. “In today's market, given the fear and uncertainty, we're looking for things to get the market flow going again.”

The likelihood of a payout is probably slim. Charlotte never had a big bubble market surge in home prices. A specific neighborhood might have had a big run-up and may fall hard. But the refund is based on the index, which as of November showed Charlotte-area prices had declined 5.3 percent compared with a year ago. That was the biggest annual drop in more than 20 years of available data.

December figures are due Tuesday.

The refund offer is backed by the company, not insurance or an outside party. So, Killian said: “It's only as good as the financial strength of the company.”

Killian said the company offers customers its credit report, prepared by an outside firm, and a financial bill of health from an accounting firm. Simonini also provides customers with contacts at 12 of its vendors, so they can confirm the builder is paying its bills.

The firm, which traces its Charlotte roots to 1973, typically builds at the higher end, with some houses above $1 million. Models opened this week at its Christenbury Hall near Concord Mills, with prices starting around $675,000. Other projects include Heydon Hall, near Quail Hollow Country Club; the SouthPark area's Conservatory, which starts around $875,000, and The Preserve at Robbins Park near Lake Norman, starting at about $645,000.

Simonini is also tackling the problem of would-be customers who can't buy because they can't sell what they have. The builder will help identify Realtors who have been successful in that area, with close attention to how closely sales prices are tracking with asking prices. Simonini interior designers will evaluate the existing house and recommend fix-ups to lure buyers. The builder will then do up to $15,000 of repairs and improvements at cost, with no profit mark-up. The customer gets the amount spent as a credit on the new home deal.

“We're in the business of selling homes,” Killian said. “We recognize there's a lot of confusion and fear in the market.”

Source

Ray Killian Jr., CEO and Director of Simonini Builders of Charlotte.One reason houses aren't selling is that people are worried prices will drop further.

A Charlotte homebuilder is offering an unusual incentive to help offset that concern.

Simonini Builders will refund customers up to 5 percent of what they paid for a house if Charlotte-area home values take a steep plunge. The refund kicks in if values decline within a year of purchase by more than 10 percent and up to 15 percent, based on a widely used home price index.

On a $700,000 house, the refund would be $700 for a decline of 10.1 percent, to as much as $35,000 if values fall 15 percent.

“We view it more as an insurance policy for the consumer,” said Ray Killian Jr., CEO and co-owner of the company. “We give them a hedge.”

For more than a year, new home construction has been plunging locally and nationwide as lending standards tightened, foreclosures glutted the market, unemployment rose and the economy soured. Even people with good credit and relatively secure jobs are hesitant to spend. And the ongoing decline in home values has some buyers holding out for lower prices or unwilling to buy and risk a quick loss.

Discounting and other incentives have been common among builders hungry for sales. Killian says they've already cut prices 8 percent to 13 percent.

But several real estate experts said they hadn't heard of a refund plan like the Simonini deal. The hedge, which Killian credits to Chief Financial Officer Bill Saint, is based on the widely watched S&P/Case-Shiller Home Price Index.

“It's a very clever idea,” said François Ortalo-Magné, a professor and chairman of the real estate department at the University of Wisconsin-Madison. “In today's market, given the fear and uncertainty, we're looking for things to get the market flow going again.”

The likelihood of a payout is probably slim. Charlotte never had a big bubble market surge in home prices. A specific neighborhood might have had a big run-up and may fall hard. But the refund is based on the index, which as of November showed Charlotte-area prices had declined 5.3 percent compared with a year ago. That was the biggest annual drop in more than 20 years of available data.

December figures are due Tuesday.

The refund offer is backed by the company, not insurance or an outside party. So, Killian said: “It's only as good as the financial strength of the company.”

Killian said the company offers customers its credit report, prepared by an outside firm, and a financial bill of health from an accounting firm. Simonini also provides customers with contacts at 12 of its vendors, so they can confirm the builder is paying its bills.

The firm, which traces its Charlotte roots to 1973, typically builds at the higher end, with some houses above $1 million. Models opened this week at its Christenbury Hall near Concord Mills, with prices starting around $675,000. Other projects include Heydon Hall, near Quail Hollow Country Club; the SouthPark area's Conservatory, which starts around $875,000, and The Preserve at Robbins Park near Lake Norman, starting at about $645,000.

Simonini is also tackling the problem of would-be customers who can't buy because they can't sell what they have. The builder will help identify Realtors who have been successful in that area, with close attention to how closely sales prices are tracking with asking prices. Simonini interior designers will evaluate the existing house and recommend fix-ups to lure buyers. The builder will then do up to $15,000 of repairs and improvements at cost, with no profit mark-up. The customer gets the amount spent as a credit on the new home deal.

“We're in the business of selling homes,” Killian said. “We recognize there's a lot of confusion and fear in the market.”

Source

February 21, 2009

Foreclosure silver lining: Mantecans can now afford to buy a home

Tony and Crystal Davenport once thought homeownership was something that might occur after 10 years or so of marriage – if that.

“Home prices in Manteca were between $400,000 and $500,000 when we first got together,” Crystal recalled.

This month the couple moved into their own home on Wedgewood Way in north Manteca. Their home is costing them $40 a month more to buy that it did to rent a one-bedroom apartment for $1,025 a month previously at Paseo Villas.

“There is a lot more space here than in our one bedroom apartment,” Tony said as he walked through the 1,476-square-foot home that also has a two-car garage. “I can change my own oil or wash my car here. You couldn’t do that at the apartments. I can have all our friends over instead of just a few at a time.”

They are among an estimated 600 to 900 Manteca families in the past 13 months who have gone from renting to buying a home thanks to the affordability index that hasn’t been this high since the early 1970s once income and housing prices are factored into the equation. There have been 1,296 resale homes sold in Manteca during the past 13 months with investors buying up what buyers who are looking to own to live in a home don’t purchase.

Based on trends over the years, 2008 arguably was the best year for Manteca-based buyers in sheer numbers since the 1970s as both those buying to live in homes or buy them as an investment dominated the local market that up until the foreclosure crisis was comprised primarily of those coming out of the Bay Area with fatter paychecks.

Many of those taking the plunge are couples and individuals in their 20s who came of age believing buying a home in Manteca would be next to impossible for them to do. The Davenports thought it was out of the question for them since they have a baby on the way and Crystal is going to school full-time in addition to a full-time job in retail.

“We didn’t want to raise our baby in an apartment,” Tony, 24, said.

Couple beats out another buyer

The couple started out in December working with Realtor Tom Wilson after getting pre-approved for a loan up to $180,000 on the strength of his full-time job with Turlock Irrigation District.

They made it clear that they wanted to leave wriggle room so things wouldn’t be so tight that they’d have to be even more careful on how they spent money than they currently were.

That brought them to Wedgewood with a $150,000 list price.

They would have preferred granite counter tops in the kitchen but they figure they will get that in time and do the work themselves for a lot less money. They ended up in a mini-bidding war. They made the offer on Christmas Eve only to have Wilson call them back to let them know there was another pre-approved buyer but that buyer was maxed out.

“We ended up getting it for just $500 more,” Tony said.

To walk through their home, you’d have a hard time visualizing that it had been trashed as a foreclosure. They said neighbors told them that there were more than a dozen holes in the walls and that other things had been damaged. You couldn’t tell that, though, after the bank got through. The interior was painted, 6-inch baseboard put in place as well as crown molding throughout. Tony has already made improvements to one bathroom in the three-bedroom home and is ready to do the master suite bathroom next.

The Davenports quickly learned that finding the “ideal house” with desired bells and whistles for a low price wasn’t realistic. One such home they were interested was available for less than the one they bought but by the time bidding got through it sold for tens of thousands more than they paid for their Wedgewood Way home.

Looking forward to paying off home

That’s fine with Tony who said he’s gotten “the new car thing” out of his system.

He noted by not going to the max of what they were approved for, they were able to buy things they needed for the house such as major appliances that they didn’t have as renters.

“I’m looking forward to the day in 30 years when I don’t have a housing payment,” he said.

Tony said he liked the idea of not “writing a check at the first of the month to send money down a hole” and that instead they were buying something to call their own.

Tony and Crystal said one of the best things besides having a place of their own that they can improve as they wish is the fact they now know what their housing costs will be each month for the next 30 years instead of worrying about rent increases.

Buying a home with what seems to be non-stop bad economic news fed by cable TV channels didn’t worry the couple.

“I figured if I lost my job I’d find some way to feed my family and (make the mortgage payments) whether it is flipping burgers, driving a diesel or whatever I needed to do,” Tony said.

Both Crystal and Tony think that anyone that is renting should check into buying as soon as possible noting that the current prices aren’t going to last forever.

At the market’s peak in 2006, the median housing price hit $443,000 in Manteca or 7.1 times the city’s household median income of $62,000. Today’s median selling price so far in 2009 is $179,900 or 2.9 times the median household income.

It reflects a trend throughout California where just three years ago less than 29 percent of households could afford to buy based on housing prices. Today, that number who can afford to own their own home if they so chose has soared to over 53 percent thanks to falling prices triggered by the foreclosure mess.

He was particularly impressed with Wilson who at the outset told them that he had no worries about feeding his children or keeping a roof over this head if he didn’t sell them a house.

“I liked hearing that,” Tony said. “I don’t like pushy people. He was upfront, no clouds, and no curtains.”

Tony said Wilson was great at helping educate them about the market. He even stepped in and checked things such as wall sockets to get an idea of a house’s electrical system’s condition. He also interceded and got the bank to replace a dishwasher that was stolen while the home was in escrow and got the bank to make repairs to the garage door.

“That’s pretty good since the home was being sold ‘as is’,” Tony noted.

The couple appreciated their families who have helped them but especially Jeff and Tevani Liotard.

They said they have no regrets and aren’t going to worry whether they bought too soon if prices even drop a little bit more.

“The home works for us,” he said, noting they’re happy with the deal, the tax advantages they’re getting, and the fact they can start building their family.

“It felt good,” Tony said when escrow closed on Jan.29 and the keys to their own home were placed in their hands. “It felt real good.”

Source

“Home prices in Manteca were between $400,000 and $500,000 when we first got together,” Crystal recalled.

This month the couple moved into their own home on Wedgewood Way in north Manteca. Their home is costing them $40 a month more to buy that it did to rent a one-bedroom apartment for $1,025 a month previously at Paseo Villas.

“There is a lot more space here than in our one bedroom apartment,” Tony said as he walked through the 1,476-square-foot home that also has a two-car garage. “I can change my own oil or wash my car here. You couldn’t do that at the apartments. I can have all our friends over instead of just a few at a time.”

They are among an estimated 600 to 900 Manteca families in the past 13 months who have gone from renting to buying a home thanks to the affordability index that hasn’t been this high since the early 1970s once income and housing prices are factored into the equation. There have been 1,296 resale homes sold in Manteca during the past 13 months with investors buying up what buyers who are looking to own to live in a home don’t purchase.

Based on trends over the years, 2008 arguably was the best year for Manteca-based buyers in sheer numbers since the 1970s as both those buying to live in homes or buy them as an investment dominated the local market that up until the foreclosure crisis was comprised primarily of those coming out of the Bay Area with fatter paychecks.

Many of those taking the plunge are couples and individuals in their 20s who came of age believing buying a home in Manteca would be next to impossible for them to do. The Davenports thought it was out of the question for them since they have a baby on the way and Crystal is going to school full-time in addition to a full-time job in retail.

“We didn’t want to raise our baby in an apartment,” Tony, 24, said.

Couple beats out another buyer

The couple started out in December working with Realtor Tom Wilson after getting pre-approved for a loan up to $180,000 on the strength of his full-time job with Turlock Irrigation District.

They made it clear that they wanted to leave wriggle room so things wouldn’t be so tight that they’d have to be even more careful on how they spent money than they currently were.

That brought them to Wedgewood with a $150,000 list price.

They would have preferred granite counter tops in the kitchen but they figure they will get that in time and do the work themselves for a lot less money. They ended up in a mini-bidding war. They made the offer on Christmas Eve only to have Wilson call them back to let them know there was another pre-approved buyer but that buyer was maxed out.

“We ended up getting it for just $500 more,” Tony said.

To walk through their home, you’d have a hard time visualizing that it had been trashed as a foreclosure. They said neighbors told them that there were more than a dozen holes in the walls and that other things had been damaged. You couldn’t tell that, though, after the bank got through. The interior was painted, 6-inch baseboard put in place as well as crown molding throughout. Tony has already made improvements to one bathroom in the three-bedroom home and is ready to do the master suite bathroom next.

The Davenports quickly learned that finding the “ideal house” with desired bells and whistles for a low price wasn’t realistic. One such home they were interested was available for less than the one they bought but by the time bidding got through it sold for tens of thousands more than they paid for their Wedgewood Way home.

Looking forward to paying off home

That’s fine with Tony who said he’s gotten “the new car thing” out of his system.

He noted by not going to the max of what they were approved for, they were able to buy things they needed for the house such as major appliances that they didn’t have as renters.

“I’m looking forward to the day in 30 years when I don’t have a housing payment,” he said.

Tony said he liked the idea of not “writing a check at the first of the month to send money down a hole” and that instead they were buying something to call their own.

Tony and Crystal said one of the best things besides having a place of their own that they can improve as they wish is the fact they now know what their housing costs will be each month for the next 30 years instead of worrying about rent increases.

Buying a home with what seems to be non-stop bad economic news fed by cable TV channels didn’t worry the couple.

“I figured if I lost my job I’d find some way to feed my family and (make the mortgage payments) whether it is flipping burgers, driving a diesel or whatever I needed to do,” Tony said.

Both Crystal and Tony think that anyone that is renting should check into buying as soon as possible noting that the current prices aren’t going to last forever.

At the market’s peak in 2006, the median housing price hit $443,000 in Manteca or 7.1 times the city’s household median income of $62,000. Today’s median selling price so far in 2009 is $179,900 or 2.9 times the median household income.

It reflects a trend throughout California where just three years ago less than 29 percent of households could afford to buy based on housing prices. Today, that number who can afford to own their own home if they so chose has soared to over 53 percent thanks to falling prices triggered by the foreclosure mess.

He was particularly impressed with Wilson who at the outset told them that he had no worries about feeding his children or keeping a roof over this head if he didn’t sell them a house.

“I liked hearing that,” Tony said. “I don’t like pushy people. He was upfront, no clouds, and no curtains.”

Tony said Wilson was great at helping educate them about the market. He even stepped in and checked things such as wall sockets to get an idea of a house’s electrical system’s condition. He also interceded and got the bank to replace a dishwasher that was stolen while the home was in escrow and got the bank to make repairs to the garage door.

“That’s pretty good since the home was being sold ‘as is’,” Tony noted.

The couple appreciated their families who have helped them but especially Jeff and Tevani Liotard.

They said they have no regrets and aren’t going to worry whether they bought too soon if prices even drop a little bit more.

“The home works for us,” he said, noting they’re happy with the deal, the tax advantages they’re getting, and the fact they can start building their family.

“It felt good,” Tony said when escrow closed on Jan.29 and the keys to their own home were placed in their hands. “It felt real good.”

Source

February 20, 2009

After Foreclosure: Will Your Mortgage Home Lender—Sue You To Recover Loan Losses?

“Recourse Home Mortgages" can hold borrowers personally liable for lender loses should their home be lost to foreclosure.

Alarmingly many homeowners don’t know if the loan they used to buy their home is a “Recourse Mortgage.” Recourse loans allow mortgage lenders to sue homeowners after foreclosure—to recover “loan losses” when the lender sells the foreclosed house—for less than what is owed.

Some states prohibit mortgage lenders from suing homeowners after foreclosure to recover loan losses on a “Purchase Money Mortgage” used to buy a home that was the owner’s residence. However lenders unless prohibited by law, can get “deficiency judgments” against foreclosed homeowners to recover losses incurred from refinance-mortgage loans and outstanding credit lines secured by the foreclosed residence.

Bankruptcy for some foreclosed-homeowners might be the only option to prevent persistent mortgage lenders from attaching their future income and assets.

As millions approach home foreclosure, some Americans might wonder if their own lender contributed to wiping out their home equity. That might appear true if their lender—continued to make Sub-prime mortgages to borrowers more likely to default in their neighborhood—after having actual knowledge there was a large number of home foreclosures. Many homeowners that live near foreclosed properties continue to see the value of their homes plummet.

Sub-prime mortgage lenders appear protected from homeowner and borrower plaintiffs that might allege a lender’s loan practices damaged the value of their home. Congress passed the “1977 Community Reinvestment ACT” and other laws that encouraged lenders to make higher-risk loans to less qualified borrowers to expand home-ownership in the U.S. However, there might be state and federal jurisdiction issues that “Recourse Mortgage Borrowers” can raise that concern whether a mortgage lender breached a fiduciary duty owed a client-borrower.

Banks track mortgage defaults and foreclosures. Because foreclosures are so prevalent and bring down the value of nearby properties, shouldn’t lenders that market “Recourse Mortgages”, be required to disclose to home loan borrowers the number of house foreclosures within a certain distance of the home the lender is soliciting making a Recourse loan? “Recourse Mortgages" can hold borrowers personally liable should their home be lost to foreclosure. Nevada for example is inundated with recourse loan foreclosures. It appears doubtful that all lenders clearly explained Recourse Mortgages to their client borrowers.

Source

Alarmingly many homeowners don’t know if the loan they used to buy their home is a “Recourse Mortgage.” Recourse loans allow mortgage lenders to sue homeowners after foreclosure—to recover “loan losses” when the lender sells the foreclosed house—for less than what is owed.

Some states prohibit mortgage lenders from suing homeowners after foreclosure to recover loan losses on a “Purchase Money Mortgage” used to buy a home that was the owner’s residence. However lenders unless prohibited by law, can get “deficiency judgments” against foreclosed homeowners to recover losses incurred from refinance-mortgage loans and outstanding credit lines secured by the foreclosed residence.

Bankruptcy for some foreclosed-homeowners might be the only option to prevent persistent mortgage lenders from attaching their future income and assets.

As millions approach home foreclosure, some Americans might wonder if their own lender contributed to wiping out their home equity. That might appear true if their lender—continued to make Sub-prime mortgages to borrowers more likely to default in their neighborhood—after having actual knowledge there was a large number of home foreclosures. Many homeowners that live near foreclosed properties continue to see the value of their homes plummet.

Sub-prime mortgage lenders appear protected from homeowner and borrower plaintiffs that might allege a lender’s loan practices damaged the value of their home. Congress passed the “1977 Community Reinvestment ACT” and other laws that encouraged lenders to make higher-risk loans to less qualified borrowers to expand home-ownership in the U.S. However, there might be state and federal jurisdiction issues that “Recourse Mortgage Borrowers” can raise that concern whether a mortgage lender breached a fiduciary duty owed a client-borrower.

Banks track mortgage defaults and foreclosures. Because foreclosures are so prevalent and bring down the value of nearby properties, shouldn’t lenders that market “Recourse Mortgages”, be required to disclose to home loan borrowers the number of house foreclosures within a certain distance of the home the lender is soliciting making a Recourse loan? “Recourse Mortgages" can hold borrowers personally liable should their home be lost to foreclosure. Nevada for example is inundated with recourse loan foreclosures. It appears doubtful that all lenders clearly explained Recourse Mortgages to their client borrowers.

Source

February 16, 2009

New grads might get aid to buy Ohio home

A measure that would give cash incentives for college graduates to buy a house and live in Ohio is among the priority bills for Senate Republicans over the two-year session.

Senate Bill 5 would create a $2 million annual grant program to provide recent college graduates with down-payment help on the purchase of a home in Ohio.

"If we truly want to get our economy back on track, Ohio cannot afford to lose the next generation of skilled workers to other states," said Sen. Stephen Buehrer, R-Delta, who is sponsoring the bill. "This program will provide an extra incentive for our best and brightest to purchase their own homes and become invested in our communities."

Under the proposal, Ohio residents could register within 60 days of graduating for a lottery that would award 300 grants ranging from $2,500 to $10,000 depending on the level of degree the graduate has earned. Recipients would have one year to use the grant.

Senate President Bill M. Harris, R-Ashland, said the priorities for his members also will focus on job creation and a more business-friendly regulatory environment.

Other priority bills unveiled yesterday:

• A push for quicker spending of the $1.6 billion Ohio job-stimulus bill in areas such as alternative energy, biosciences and logistics. The bill would allocate the remaining $340 million of the stimulus package for 2010-11.

• A spending blueprint for the current federal economic-stimulus package, known as the American Recovery and Reinvestment Act. Republican lawmakers are concerned that Gov. Ted Strickland will try to spend infrastructure money without going through established channels. "We must move quickly, but not at the expense of transparency, especially as we are talking about such a large expenditure of taxpayer dollars," said Sen. John A. Carey Jr., a Wellston Republican and chairman of the Senate Finance Committee.

• Regulatory reforms as proposed recently by the Regulatory Reform Task Force. This includes eliminating duplication and adjusting fees.

• Performance audits of regulatory agencies, performed by the state auditor, to gauge their progress in promoting "common sense" business regulation.

Senate Bill 5 would create a $2 million annual grant program to provide recent college graduates with down-payment help on the purchase of a home in Ohio.

"If we truly want to get our economy back on track, Ohio cannot afford to lose the next generation of skilled workers to other states," said Sen. Stephen Buehrer, R-Delta, who is sponsoring the bill. "This program will provide an extra incentive for our best and brightest to purchase their own homes and become invested in our communities."

Under the proposal, Ohio residents could register within 60 days of graduating for a lottery that would award 300 grants ranging from $2,500 to $10,000 depending on the level of degree the graduate has earned. Recipients would have one year to use the grant.

Senate President Bill M. Harris, R-Ashland, said the priorities for his members also will focus on job creation and a more business-friendly regulatory environment.

Other priority bills unveiled yesterday:

• A push for quicker spending of the $1.6 billion Ohio job-stimulus bill in areas such as alternative energy, biosciences and logistics. The bill would allocate the remaining $340 million of the stimulus package for 2010-11.

• A spending blueprint for the current federal economic-stimulus package, known as the American Recovery and Reinvestment Act. Republican lawmakers are concerned that Gov. Ted Strickland will try to spend infrastructure money without going through established channels. "We must move quickly, but not at the expense of transparency, especially as we are talking about such a large expenditure of taxpayer dollars," said Sen. John A. Carey Jr., a Wellston Republican and chairman of the Senate Finance Committee.

• Regulatory reforms as proposed recently by the Regulatory Reform Task Force. This includes eliminating duplication and adjusting fees.

• Performance audits of regulatory agencies, performed by the state auditor, to gauge their progress in promoting "common sense" business regulation.

February 12, 2009

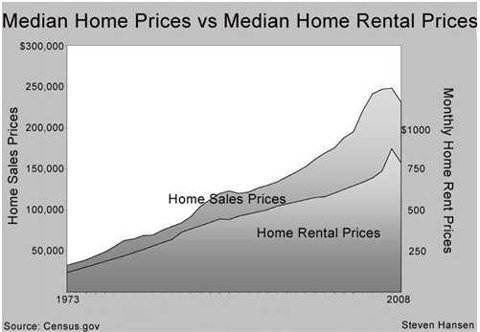

Better to Rent than Buy a Home

At the end of 2008, 57.5% of all homes were owned, 27.5% were rented, and 15% were vacant.

The difficulty in analyzing home ownership versus renting is that you are comparing apples to oranges. The median rental unit is different than the median house. The square footage per person and occupancy count is similar – but in the rentals there are a higher percentage of multi-family structures. Rental homes are skewed towards zero maintenance types with less land.

But in the years where enough data was available to ensure a relatively exact correlation – it did not appear to distort the median rental rate by more than 5% up or down. The data used in this analysis is from U.S. Census / HUD – and not from the National Association of Realtors (NAR).

Another issue in analyzing this subject is regional differences. There are areas in America relatively unaffected by the housing crisis. And in other areas, the prices have fallen by half. Even within states, there are significant differentials of data. Also, there are areas which have shortages or surpluses of rental properties which would diminish the applicability of this analysis. So in analyzing “median” data, it may not match any area in America exactly.

Looking at these graphs, there does not seem to be any financial reason to own a home – except for appreciation. This is why we buy a home. We purchase it and hold it for a period of time – then we sell it. We psychologically believe we have made a lot of money, but the reality is that the majority just buy another house – so there has been no realized gain.

The graph below shows the appreciation of home values on a monthly basis between 1973 and 2008. Home owners in the past have made significant gains to their net worth. read more

The difficulty in analyzing home ownership versus renting is that you are comparing apples to oranges. The median rental unit is different than the median house. The square footage per person and occupancy count is similar – but in the rentals there are a higher percentage of multi-family structures. Rental homes are skewed towards zero maintenance types with less land.

But in the years where enough data was available to ensure a relatively exact correlation – it did not appear to distort the median rental rate by more than 5% up or down. The data used in this analysis is from U.S. Census / HUD – and not from the National Association of Realtors (NAR).

Another issue in analyzing this subject is regional differences. There are areas in America relatively unaffected by the housing crisis. And in other areas, the prices have fallen by half. Even within states, there are significant differentials of data. Also, there are areas which have shortages or surpluses of rental properties which would diminish the applicability of this analysis. So in analyzing “median” data, it may not match any area in America exactly.

Looking at these graphs, there does not seem to be any financial reason to own a home – except for appreciation. This is why we buy a home. We purchase it and hold it for a period of time – then we sell it. We psychologically believe we have made a lot of money, but the reality is that the majority just buy another house – so there has been no realized gain.

The graph below shows the appreciation of home values on a monthly basis between 1973 and 2008. Home owners in the past have made significant gains to their net worth. read more

February 11, 2009

Confidence 'returning to market'

Consumer confidence is returning to the housing market with two-thirds of people thinking now is a good time to buy a new home, a survey has found.

Around 66% of people said they thought it was currently a good time to buy a property, but just 2.1% said it was a good time to sell one, according to property website Rightmove.

The findings suggest people think it is a buyers' market, in which those who have the funds in place to go ahead with a purchase can negotiate big discounts.

Nearly half of people who responded to a survey on Rightmove's website plan to buy a home during the coming 12 months, despite the fact seven out of 10 expect prices to fall further during the year.

In fact, potential buyers seem to have identified 2009 as the window in which to buy property, with only 38.4% thinking it will still be a good time to buy a home in 12 months' time, while just over a third of those questioned said they thought 2010 would be a good time to sell a property.

Miles Shipside, commercial director at Rightmove, said: "With interest rates at historic lows and set to fall further, and property deals available at around 25% below peak boom prices, buying has got a whole lot cheaper.

"Other assets now seem a lot less solid than bricks and mortar, so the time-to-buy pendulum is swinging from negative to positive.

"It's aided by some homeowners' mortgage repayments being the lowest they have ever experienced and the prospect of them getting even cheaper - a real turnaround from just a few months ago."

Around 16% of the 28,212 people questioned said they would be willing to borrow more than four times their salary to buy a home, even though tighter lending criteria mean they may not be able to do this, although 49% of people are more wary and said they would only borrow up to three times their pay.

Meanwhile, property website Mouseprice.com said there was a continuing stand-off between buyers and sellers, as homeowners refused to accept how far the value of their home had fallen.

Source

February 10, 2009

Senate approves $15,000 home purchase tax credit

The Senate today passed a tax credit of up to $15,000 for anyone who buys a house this year. The proposal was pushed by Republicans who favored targeted tax credits over no-strings rebates.

There's currently a $7,500 tax credit for home purchases, but the money must be repaid.

The Senate measure, if it becomes law, would provide a credit of 10% of the home purchase price, up to a maximum credit of $15,000.

Real estate industry groups have backed such a credit as a way to spur demand for homes.

Source

There's currently a $7,500 tax credit for home purchases, but the money must be repaid.

The Senate measure, if it becomes law, would provide a credit of 10% of the home purchase price, up to a maximum credit of $15,000.

Real estate industry groups have backed such a credit as a way to spur demand for homes.

Source

February 2, 2009

Fannie and Freddie's new home loan rules - you need lots of cash

We've all heard that it's getting harder and harder to qualify for a new loan, but no one's been certain exactly what Fannie Mae and Freddie Mac have set as rules in this new financial environment.

In a story in today's Wall Street Journal, we find that a borrower needs a credit score of at least 740 to qualify for a home-purchase loan with a 20% down. With that excellent credit score the borrower could qualify for a loan rate of 4.75% plus a 1% origination fee. If a borrower's credit score is below 680, then the best he or she could do would be a 4.75% loan with 2.5% in fees.

So what do you need in cash to buy a home today using Fannie or Freddie? if you've got a score of 740 or higher and want to buy a home valued at $200,000, you would need to have $40,000 to put down on the home plus another $2,000 for fees before you could even think about buying. If your credit score was below 680, you would need the $40,000 down plus $5,000 in fees.

The only way you might find a way to purchase a home with less cash up front would be to work with the FHA. The FHA is still accepting borrowers with low credit scores and down payments of as little as 3.5%.Fannie and Freddie say they are focusing on keeping people in their homes and not on making new loans. The problem is that since Frannie and Freddie are the only players in town for most mortgages, since private mortgage money dried up, there's not much to go around to help people who want to buy a home. The only way we're going to stop the downward spiral in home prices is to reduce the backlog of homes on the market. read more

February 1, 2009

UPDATE: Furniture, bedding groups seek tax incentives

To provide a boost to the home furnishings industry, several industry trade associations are asking Congress and the new Obama administration for tax incentives to offset product purchases and home improvements and help industry companies.

The American Home Furnishings Alliance, the International Sleep Products Assn. and the National Home Furnishings Assn. are proposing a two- to three-year refundable tax credit for the purchase or installation of home furnishings.

A credit of 10% to 20% would be available to renters or homeowners making $50,000 or less. The proposal also includes a 10% tax deduction, capped at $2,000, for furniture purchases for individuals with incomes under $150,000 and for couples with incomes under $250,000.

Commercial, retail and contractor incentives would include:

+ A 10% refundable tax credit for inventory purchases of building products.

+ A tax deduction for bad debt based on historical experience, rather than when the debt is proven to be uncollectible.

+ A capped tax credit for commercial and investor taxpayers on the purchase of building products otherwise considered to be ordinary and necessary building expenses, such as paint.

+ A 50% bonus depreciation in the year of purchase for depreciable building products for commercial and investor taxpayers.

Other trade groups supporting the incentives include the Carpet and Rug Institute, the Kitchen Cabinet Manufacturers Assn., the National Paint and Coatings Assn, the Resilient Floor Covering Institute and the World Floor Covering Assn. The groups call themselves the American Home Furnishings and Building Products Coalition.

"Incentives for the purchase of home furnishings and building products will help boost the housing market, help low and middle income taxpayers, and directly protect American manufacturing and retail jobs," AHFA CEO Andy Counts said in a statement.

The groups project that the incentives would help generate $128 billion for the U.S. economy over two years and also would generate 352,000 U.S. jobs in retail, manufacturing and contractor services. Of the total, the incentives are expected to generate a combined $102 billion for home remodeling and other home improvements and $26.2 billion in home furnishings product sales. read more

The American Home Furnishings Alliance, the International Sleep Products Assn. and the National Home Furnishings Assn. are proposing a two- to three-year refundable tax credit for the purchase or installation of home furnishings.

A credit of 10% to 20% would be available to renters or homeowners making $50,000 or less. The proposal also includes a 10% tax deduction, capped at $2,000, for furniture purchases for individuals with incomes under $150,000 and for couples with incomes under $250,000.

Commercial, retail and contractor incentives would include:

+ A 10% refundable tax credit for inventory purchases of building products.

+ A tax deduction for bad debt based on historical experience, rather than when the debt is proven to be uncollectible.

+ A capped tax credit for commercial and investor taxpayers on the purchase of building products otherwise considered to be ordinary and necessary building expenses, such as paint.

+ A 50% bonus depreciation in the year of purchase for depreciable building products for commercial and investor taxpayers.

Other trade groups supporting the incentives include the Carpet and Rug Institute, the Kitchen Cabinet Manufacturers Assn., the National Paint and Coatings Assn, the Resilient Floor Covering Institute and the World Floor Covering Assn. The groups call themselves the American Home Furnishings and Building Products Coalition.

"Incentives for the purchase of home furnishings and building products will help boost the housing market, help low and middle income taxpayers, and directly protect American manufacturing and retail jobs," AHFA CEO Andy Counts said in a statement.

The groups project that the incentives would help generate $128 billion for the U.S. economy over two years and also would generate 352,000 U.S. jobs in retail, manufacturing and contractor services. Of the total, the incentives are expected to generate a combined $102 billion for home remodeling and other home improvements and $26.2 billion in home furnishings product sales. read more

Subscribe to:

Posts (Atom)